The SEC is seeking public input for a new proposed rule, Enhancement of EGC Accommodations and Filer Status Simplification for Reporting Companies, that would radically change the existing disclosure requirements and filer statuses for most public companies.

In my recent blog, we explored the new SEC proposal to make semiannual reporting an option for public companies rather than the current mandated quarterly reports. The two proposals are designed to work hand in hand to decrease the burden for reporting companies and encourage more companies to go public. When the SEC proposed the latest rule on May 19, 2026, SEC Chair Paul Atkins suggested, “By expanding existing benefits to more companies, simplifying the analysis required for a company to avail itself of those benefits, and enhancing certainty of how long a company receives them, the Filer Status Proposal would make public company status more attractive.” The SEC designed the semiannual reporting and filer status proposals with these goals in mind to work in conjunction with the Registered Offering Reform proposal which I’ll review in my next post.

Overview of the proposal

Today, public companies are categorized into five overlapping and tangled filer statuses, each with their own requirements and accommodations:

- Large Accelerated filers (“LAF”)

- Accelerated filers (“AF”)

- Non-Accelerated filers (“NAF”)

- Smaller reporting companies (“SRC”)

- Emerging growth companies (“EGC”)

Overall, the new proposal would:

- Extend the accommodations that Emerging Growth Companies (EGCs) receive to more filers and

- Modify the existing Filer status categories to ease reporting for more public companies.

The proposed filer status changes would affect the filing deadlines and disclosures discussed in the semiannual reporting proposal. Under the new proposal, just over 80 percent of all existing SEC reporting companies will become Non-Accelerated filers while less than 20 percent would be eligible for the most seasoned status of Large Accelerated Filers.

Key highlights of the proposed rule

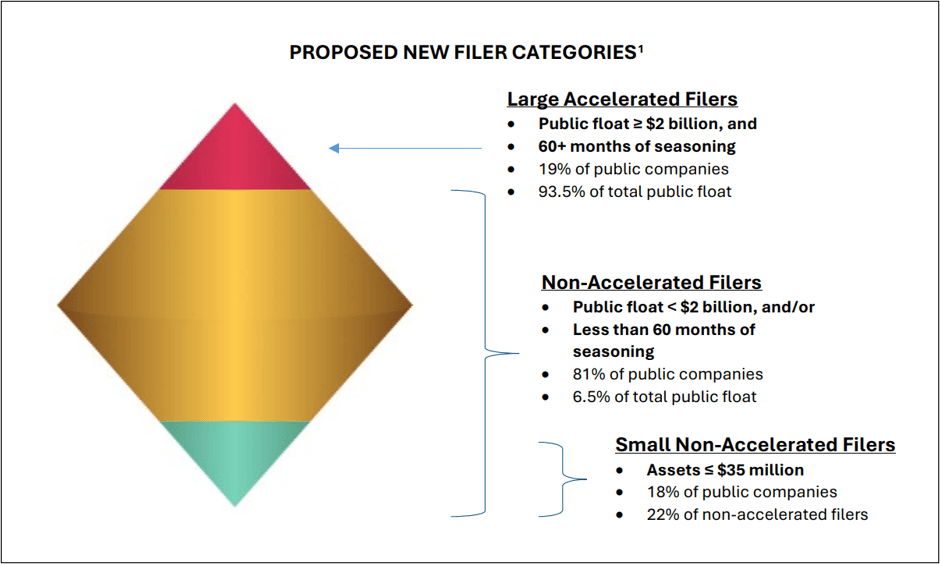

1. The SEC would reduce today’s filer framework into two main categories:

- Large Accelerated filers (LAF)

- Non-Accelerated filers (NAF)

- New sub-category for small non-accelerated filers (SNF). Companies with total assets of $35 million or less for the two most recent years would qualify. This group would receive even more timing relief on periodic reports:

- An additional 30 days to file Form 10-K annual reports, and

- An additional five days to file Form 10-Q quarterly reports.

- New sub-category for small non-accelerated filers (SNF). Companies with total assets of $35 million or less for the two most recent years would qualify. This group would receive even more timing relief on periodic reports:

Under the proposal, the accelerated filer and smaller reporting company categories would be eliminated.

2. The threshold to become a large accelerated filer would increase dramatically

The SEC proposes raising the public float threshold for large accelerated filer status from the current $700 million to $2 billion. The proposal would also calculate public float using the average stock price over the last ten trading days of the second fiscal quarter, rather than relying on a single measurement-date price. This is designed to reduce volatility in filer status determinations and make status changes less sensitive to short-term stock price swings.

3. Companies would need more seasoning before becoming a large accelerated filer

The proposal would require a company to have been subject to Exchange Act reporting for at least sixty consecutive calendar months (five years) before it could become a large accelerated filer. It would also require the public float threshold to be met for two consecutive years, so a single-year spike would not push a company into LAF status.

4. Most non-accelerated filers would receive broader disclosure accommodations

One of the most consequential pieces of the proposal is that the SEC would extend to all non-accelerated filers many of the existing accommodations that are currently reserved for smaller reporting companies and emerging growth companies, including:

- Scaled executive compensation disclosure;

- No pay-versus-performance (PVP) disclosure;

- No say-on-pay or say-when-on-pay shareholder advisory votes;

- Fewer years of financial statements and reduced presentation requirements; and

- Broader use of accommodations that today are available only to SRCs and EGCs.

5. Non-accelerated filers would not be subject to the ICFR auditor’s attestation requirement

Under the proposal, non-accelerated filers would not be required to obtain an auditor’s attestation on internal control over financial reporting (ICFR). Under the new framework, since more companies would fall into the NAF category, more companies would fall outside the Section 404(b)-style auditor attestation requirement.

This is likely to be one of the proposal’s most closely watched provisions because ICFR auditor attestation is often cited as a significant compliance cost, particularly for smaller issuers. The SEC discusses both the concerns about the burden on small companies and the investor-protection tradeoffs in the release.

Filer status assessment and timing under the proposal

Recognizing that companies will need a clear path under the new requirements, the SEC proposed a transition timeline. Existing registrants would assess their LAF or NAF status as of the end of their fiscal year prior to the effectiveness of the final rules, based on public float and, where applicable, total assets, for that fiscal year and the immediately prior fiscal year.

Importantly, for this initial assessment, a registrant would not carry over its prior filer status. A company that was a large accelerated filer before the amendments would treat itself as “not currently a large accelerated filer” when applying the new definitions. A registrant that newly qualifies as an NAF could begin using the NAF scaling and accommodations in its next Securities Act or Exchange Act filing after completing the assessment. SNF registrants could begin using the extended deadlines with their next Form 10-Q or Form 10-K (or Form 10-S, if adopted).

Registrants would be permitted to complete the assessment at any time after the final rule becomes effective, but no later than the day before the last day of the fiscal year in which the rules go into effect. After this initial transition assessment, filers would return to determining their float annually as of the second fiscal quarter, using the last ten trading days, where applicable.

The SEC provides a sample timeline to help illustrate the mechanics and timing. Assuming a 12/31 FYE filer and a hypothetical Jan. 15, 2027, rule effectiveness date:

- Dec. 31, 2026 – Fiscal year end used as the assessment reference date

- Jan. 15, 2027 – The final rule becomes effective; filers may begin determining their new status

- Dec. 30, 2027 – The latest date by which filer status must be determined (at least one day before fiscal year end)

- Jan. 1, 2028 – The new status applies going forward

A registrant may take advantage of its new status as soon as that status has been determined.

What is next?

This is currently only a proposed rule. The public comment period goes through July 20, 2026. Comments may be submitted here.

How Toppan Merrill can help

Toppan Merrill is here to help you comply with the ever-changing landscape of SEC disclosure requirements. Contact us at [email protected] or by calling 800.688.4400 to speak with one of our dedicated SEC Reporting experts.

SEC resources

- SEC proposing release: https://www.sec.gov/rules-regulations/2026/05/s7-2026-18#33-11419proposed

- Fact sheet: https://www.sec.gov/files/33-11419-fact-sheet.pdf

- Proposed rule text: https://www.sec.gov/files/rules/proposed/2026/33-11419.pdf

- Submit a comment: https://www.sec.gov/comments/s7-2026-18/enhancement-emerging-growth-company-accommodations-simplification-filer-status-reporting-companies

- View public comments: https://www.sec.gov/rules-regulations/public-comments/s7-2026-18