Let’s get started

Built on the Microsoft 365® platform, Bridge integrates seamlessly and intuitively with the tools you already use, and provides a single source for your EDGAR and iXBRL submissions.

Leverage 55+ years of experience and deep global expertise to successfully navigate the regulatory disclosure process.

Expert technology. Dedicated service.

Interactive SEC Filing Deadline Calendar

Designed exclusively for public corporations and investment management companies. Simply enter your filer status, FYE and form types to view key filing dates.

Access the calendar

Speed, Accuracy and Expertise for Corporate Compliance

Bridge is expert software, coupled with dedicated EDGAR and iXBRL filing consultants that work directly with your reporting team to make disclosure content management easier, faster and more accurate.

A truly hassle-free, optimal approach to financial content management and SEC compliance reporting. Create, manage and perfect disclosure content with speed and accuracy, then transmit outputs directly to the SEC and other global regulatory bodies.

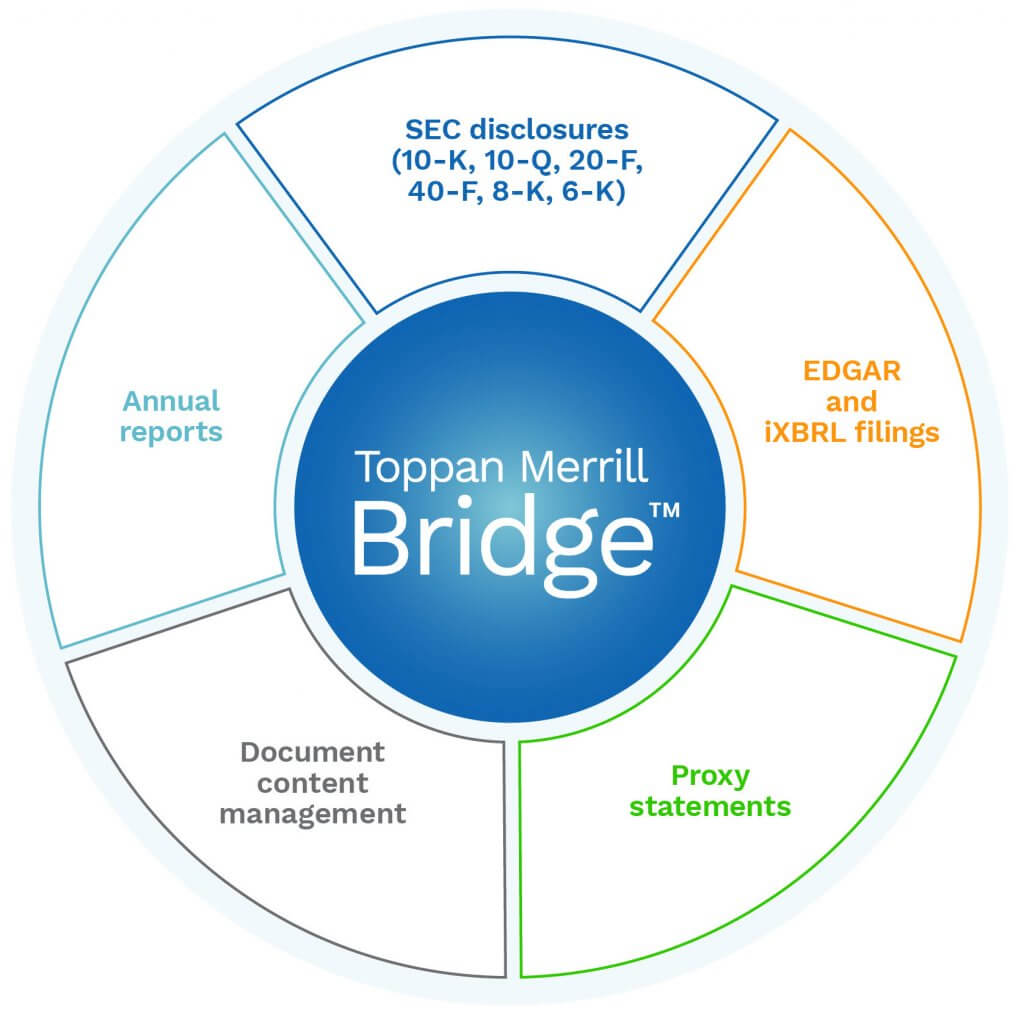

Count on Bridge for:

- Document content management

- SEC disclosures (10-K, 10-Q, 20-F, 40-F, 8-K, 6-K)

- EDGAR and iXBRL filings

- Proxy statements

- Annual reports

Productivity unlocked

Expertise that matters

Features and Functionality

Intuitive and Integrated Platform

- Integrates seamlessly and intuitively with Microsoft 365®

- Connect Excel® data directly to your disclosure document either from your desktop or network drive

iXBRL/XBRL Tagging and Review

- Integrated XBRL viewer for validation

- XBRL tagging and approval functionality

Collaborative and Transparent

- Section lock functionality for exclusive control while editing

- Edit and version history tools to track changes

Global Compliance Disclosure Solutions

- Direct connection to the SEC for EDGAR HTML and iXBRL submissions

- US GAAP and IFRS Taxonomy integrations

Efficient and Accurate

- iXBRL preview of multiple XBRL-tagged documents in a submission

- Excel® and PowerPoint® data linking functionality to reflect latest changes

Safe and Secure

- ISO 27001:2013 certified and SOC 2 Type II compliance

- Two-factor authentication, user-selected security questions and login history

On The Dot

Podcast: SEC Section 16 requirements for Foreign Private Issuers beginning March 18, 2026 [7:27]

On The Dot (Episode 13) – A conversation with Jennifer Froberg on the new requirement for officers and directors of Foreign Private Issuers to comply with SEC Section 16 reporting beginning March 18, 2026.

Updates and Insights

The shift from annual updates to always-on communication: How leading companies strengthen shareholder communication and investor relationships

Redefining the SEC compliance reporting cadence: Inside the SEC’s Semiannual Reporting proposal

New SEC Section 16 requirements for Foreign Private Issuers

Related Solutions

SEC Reporting and Filing Software

Annual Meeting & Proxy Solutions

Contact our team to get started.

Phone

Have more questions?

Reduce complexity and get answers to some of our customers’ frequently asked questions.

See the full list of FAQsEDGAR (Electronic Data Gathering, Analysis, and Retrieval) is the automated, online system the SEC provides for the receipt, acceptance, review and dissemination of documents submitted in electronic format from the SEC. The EDGAR site is free to the public for searching and viewing corporate regulatory filings on the web or via File Transfer Protocol (FTP).

The SEC implemented EDGAR to improve efficiency and transparency around corporate filings. All publicly traded companies use EDGAR to submit required, time-sensitive documents to the SEC.

Documents that must be filed via EDGAR include annual and quarterly statements, tender offers, information regarding institutional investors’ holdings, Schedule 13D and other key filings, many of which are the most important to investors and analysts. Except in the case of investment companies, actual annual reports to shareholders don’t need to be submitted on EDGAR, although some companies do so voluntarily.

Filers must submit various official EDGAR filings in Interactive Data format, using Inline XBRL (iXBRL). EDGAR was phased into use over a three-year period ending May 6, 1996. Consequently, filings from that date and earlier may not be included in the system due to a hardship exemption made for hardcopy paper filings. For support and additional information, explore our SEC reporting solutions.

GAAP is an acronym for Generally Accepted Accounting Principles, the standard accounting recording and reporting procedures used to compile financial statements to meet U.S. industry standards and regulations. The US GAAP taxonomy aims to ensure consistency in financial reporting so that investors can better assess financial statements for investment purposes.

Through complex guidelines, GAAP sets out rules covering the fine details of financial statements, from balance sheet classification to revenue recognition. These guidelines are codified in the GAAP Taxonomy Architecture, which serves as the basis for XBRL.

Some financial accounting inconsistencies remain, however. Although U.S. companies follow GAAP rules, other countries apply London-based International Financial Reporting Standards (IFRS). This gap in standards affects global business practices, from accounting to stock market valuations.

Efforts are currently underway by the SEC to adopt IFRS standards and resolve conflicts and confusion in international financial reporting in cooperation with the International Accounting Standards Board (IASB). For support and additional information, explore our SEC reporting solutions.

The IFRS Taxonomy is a list of elements, and their relationships, which reflect the presentation and disclosure requirements of the International Financial Reporting Standards (IFRS). These elements, or tags, are used to mark-up IFRS financial statements so they can be communicated in a standardized, computer-readable format. For investment or insurance companies, or corporations, the requirements are different but the importance is high for each.

IFRS is a set of accounting principles initially outlined to harmonize EU practices. IFRS has become a de facto global accounting standard. Since 2001, the International Accounting Standards Board (IASB) has taken responsibility for codifying and developing IFRS principles to achieve the harmonization necessary to support global financial reporting.

The IASB also develops and maintains the IFRS Taxonomy, which is similar to a dictionary of financial reporting items. By selecting tags from the IFRS Taxonomy which match the related disclosures in the company’s IFRS financial statements, the company is able to prepare computer-readable financial statements in an XBRL (eXtensible Business Reporting Language) format, which is required by various regulators. For support and additional information, explore our corporate compliance solutions.